1. Name of entrepreneur/Name of entrepreneur's business/complete address (including zip code)?

Intiasar Ziyad, Fashion Stylist, www.pincklutch.com

2. Type of business organization? Pinc Klutch; www.pincklutch.com

3. Length of time the business has been in operation. 5 years.

4. List products provided by the business (goods and/or services). Fashion styling for print, high-fashion and commercial photos, periodicals, television, film, music video; wardrobe consulting and maintenance; personal shopping.

5. Number of employees/skills needed to work in the business. I am my only employee, however I do have interns to assist when needed. Interns need to be interested in the business of fashion/ wardrobe styling and I generally only take serious student who are currently in college or recently graduated (majoring in fashion merchandising or design).

6. List benefits of business to community/What does this business provide that similar businesses don’t provide. Many people aren't aware of how important image is. In business it is of the utmost importance- aside from education and experience. Unfortunately, our culture places judgment very easy and fast...that's why you often hear the phrase "first impressions are everything." It's not all about the glitz and the glam...some people aren't aware of how to be presentable in the work place or even how to "jazz it up" for business social events. My specialty is image therefore, helping businesses and individuals grow by enhancing their image is ultimately how my business benefits the community.

7. Major competitor for this business and how this business remains competitive. Local fashion stylist and designers.

8. Describe methods used to increase growth of business and any future plans for expansion.Networking. 90% of my clients come from word of mouth...therefore, by getting out to all the fashion events and shows I meet many people who are either influential in my industry or in need of my services.

9. Three greatest challenges in operating the business.(1) Maintaining a consistent income and clientele: Money isn't exactly guaranteed monthly. Because I am a freelance stylist, I sometimes have 3 or more jobs a month-other times I have 1-2 a month. (2) Finding the needed look: It is my job to maintain and keep a good relationship with local boutiques and designers to borrow or buy wardrobe. (3) Getting celebrity clientele: while it's fairly easily to get to work with C- and D-list celebrities...you haven't quite made it as a stylist until you have worked with A-and B-list celebrities, in which I have yet to do. I have come very close but my location prevents me from getting business in California and New York, which are two of several places where there tons of celebrities and work.

10. Three greatest rewards in operating the business.(1) Doing what I love...creating art with fashion & improving self esteem and image through fashion. (2) Meeting and working with talented models, photographers, hair stylist and MUA's (makeup artist). (3) The pay can be great!

Intiasar Ziyad Fashion Stylist

www.pincklutch.com

intiasar@pincklutch.com

404.384.2507

Personal Reflection on your own thoughts about the business and the business owner? I think that the business is great and it was a success. The business owner Intiasar Ziyad is a wonderful entrepreneur and had a lil help from her family but her business has been going on for 5 years and is a success.

Wednesday, October 6, 2010

Tuesday, October 5, 2010

1. Students use the format below to compare and contrast Monopoly and Oligopoly; Monopolistic Competition and Pure Competition. Must include at least 2 characteristics for each. Provide two examples for each type of company.

Monopoly Oligopoly

Similarities

1. Consumers are at a distinct price disadvantage in both conditions, as prices for products are dictated by a single company in a monopoly environment and commanded by only a few select merchants in an oligopoly condition.

2. They both have significant barriers entry’s

Differences

1. Monopoly does severely restrict consumer choices, oligopoly conditions do allow for some competition among the major players.

Monopoly Oligopoly

Similarities

1. Consumers are at a distinct price disadvantage in both conditions, as prices for products are dictated by a single company in a monopoly environment and commanded by only a few select merchants in an oligopoly condition.

2. They both have significant barriers entry’s

Differences

1. Monopoly does severely restrict consumer choices, oligopoly conditions do allow for some competition among the major players.

2. Oligopolies are a common market condition while monopolies are forbidden under federal regulations.

Monopolistic Competition Pure Competition

Similarities

1.Firms are responsive to changes in demand conditions.

2. Competition in the pursuit of profit encourages resources movements that are efficient.

Differences

1.Perfectly competitive firms don’t advertise because everyone knows the products are all the same. Monopolistic Competitor advertise to convince consumers that their product is better than others.

Reflections: What two questions do you have about this assignment?

- When a monopoly does occur?

- What are the essential features of monopoly?

Include two relevant visuals

Thursday, September 23, 2010

Standard M12 Supply and Demand Blog 5

Microeconomics

1. Using the typical 'Facebook' lingo, write a definition for Microeconomics and then provide a standard English translation for your 'Facebook' definition. Is a branch that studies how the individual parts of the economy, the household and the firms make decisions to allocate limited resources, typically in markets where goods or services are being bought and sold. Microeconomics examines how these decisions and behaviours affect the supply and demand for goods and services.Role of Money -M11

1. Using what you learned about the three functions of money, explain how 'play money' differs from 'real' money? By Using what we learned about the three functions of money, Real money is a medium of exchange, unit of account, and a store of value. Play money doesn't has any of these characteristics.

2. Money has no actual value other than the value we attach to it. The barter system would still be practiced today if the participants did not agree to set a value on a piece of printed paper that represented the value of the goods and services they had to offer. What would you accept in place of money, if someone wanted to 'buy' your most prized material possession? I would accept anything they offer me as long as it value.

2. Money has no actual value other than the value we attach to it. The barter system would still be practiced today if the participants did not agree to set a value on a piece of printed paper that represented the value of the goods and services they had to offer. What would you accept in place of money, if someone wanted to 'buy' your most prized material possession? I would accept anything they offer me as long as it value.

Circular Flow Model - M11

1. What does a circular flow model tell us? What the circular flow model tells us is that three basic elements of the economy will work and interact together to ensure that our needs and wants are provided for.

4. What is the role of government in the three sector circular flow model? The government supplies services to houses and income. They also give services and payments to businesses.

5. What role do households have in the factors or resource market (inputs)? They household factors are the four factors of production.

2. What is the role of households in the three sector circular flow model? Households provide businesses with payments in exchange for jobs and goods and services. They also pay taxes to the government and hold the four factors of production.

|

3. What is the role of businesses in the three sector circular flow model? Businesses provide income, goods, and services to households. They also pay taxes, supply goods and services to the government.

4. What is the role of government in the three sector circular flow model? The government supplies services to houses and income. They also give services and payments to businesses.

5. What role do households have in the factors or resource market (inputs)? They household factors are the four factors of production.

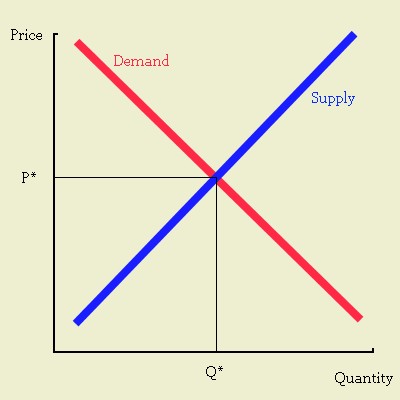

1. For each event described below, explain what happens to either the demand or supply curve. (increase/decrease, Shifts left or right?)

{kind=link}

(a) What happens to the demand for chicken if concerns about mad cow disease lead to widespread euthanizing of cows on U.S. cattle farms? The demand for chicken rises because it is a good substitute for beef and cows are becoming less and less.

(b) What happens to the supply of orange juice if Florida is hit with very severe weather? The supply of oranges will decrease and there will be no orange to make no orange because of the severe weather.

(c) In the market for coffee, severe global weather systems destroy 30% of the coffee bean crop. If the severe global weather destroy 30% of the coffee bean crop then the supply of the coffee will decrease to a low rate and there will be less coffee to sell.

(d) In the market for cereal, if the price of cardboard material used to package cereal increases. The supply will decrease unless the consumers are willing to pay more money .

2. For each part below, EXPLAIN what happens to equilibrium quantity and price (increase or decrease?).

(b) What happens to the supply of orange juice if Florida is hit with very severe weather? The supply of oranges will decrease and there will be no orange to make no orange because of the severe weather.

(c) In the market for coffee, severe global weather systems destroy 30% of the coffee bean crop. If the severe global weather destroy 30% of the coffee bean crop then the supply of the coffee will decrease to a low rate and there will be less coffee to sell.

(d) In the market for cereal, if the price of cardboard material used to package cereal increases. The supply will decrease unless the consumers are willing to pay more money .

2. For each part below, EXPLAIN what happens to equilibrium quantity and price (increase or decrease?).

a) In the market for doughnuts, if they were found to be a major contributor to high cholesterol in adults. equilibrium quantity Demand and supply will drop resulting in a new equilibrium quantity.

b) In the market for doughnuts, if widespread unemployment continues. A shift in supply to the left because there will be less doughnuts that will be produced and the price will drop on them.

c) In the market for doughnuts, if Krispy Kreme introduces a new whole wheat 'low-calorie' doughnut. The demand curve and supply curve will shift to the right resulting in a higher equilibrium quantity price.

3. What are two factors that can change the quantity demanded? Provide an example for each. 1. A change in consumers in come: an increase (decrease) in income shifts the demand curve to the right (left). 2. Population change: an increase (decrease) in population shifts the demand curve to the right (left).

4. What are two factors that can change the quantity supplied. Provide an example for each. A change in the inputs: an increase (decrease) in the input. The number's of buyers goes up or down and more suppliers enter the market.

Reflection: What are two questions that you have about standards M11 and M12.

1) How supply shocks affect supply and demand curves.

2)

Monday, September 13, 2010

Blog #4

1. How are the economic goals of freedom, security, efficiency, equity, stability, and economic growth achieved in a market economy? Freedom is the freedom of the marketplace; security is enhanced by individual efforts, such as saving and the purchase of insurance, as well as by the growth of the economy; efficiency possesses productive efficiency in producing goods; equity can be described as the application of our concepts of what is fair and what is unfair; stability is absence of inflation or deflation, not the absence of changes in relative prices in particular markets; economic growth producing increasing amounts of goods and services over the long term.

2. Why has the role of government in the economy increased dramatically since the 1880s? During the 19th century, governments played a central and pervasive role both in establishing the economic and institutional conditions necessary for the occurrence of the Industrial Revolution and for promoting its spread to the follower European nations. Everywhere, governments reduced the risks of private transactions by promulgating laws that limited entrepreneurial liability, increasing the security of property rights, and enforcing private contracts.

3. Write an argument that supports or opposes the statement in the visual below that says, "deregulation won't work because people are greedy”? I believe that the deregulation wont work, because the whole purpose of starting a business is to make money. Its very little people who can say they have enough money, because you can never have enough money. And without the regulation prices will be through the roof and the workers will be mistreated an it wouldnt benefit the consumers or owner.

4. Explain why the government provides public goods and services. Why are these public goods and services NOT provided by the private sector? (Please include a discussion on non-rivalries and non-excludable goods) The government provides public good and services because they have to be non-rivalrous and non- excludable so that everyone can have access to these goods. If private sectors provided these goods, they would not be non-rivalrous and non-excludable.

5. What are the 6 functions of government in a market economy (provide an example of how the government fulfills each of these 6 functions)? The six functions of government in a market economy are freedom, security, efficiency, stability, equity, and economic growth. Freedom is achieved by the people having the freedom to work (or not), freedom to produce, trade and consume any goods and services acquired without the use of force, fraud or theft. Security is achieved by having stable income or other resources to support a standard of living now and in the foreseen future. Efficiency is achieved by production proceeding at the lowest possible per-unit cost. Stability is achieved by the absence of excessive fluctuations in the economy, an example is high employment. Economic growth is achieved when a nation’s wealth increases over time.

6. Describe the relationship that inputs and outputs have on productivity? The input is adding more capital to a business to increase the workers productivity, which will improve the business output. In additional to that also increase the company's profit.

7. How do investments in capital goods, technology, human capital, training, and educating workers, improve productivity and economic growth? You invest into capital goods, technology, human capital, training, and educating workers that improves productivity because smarter workers find ways to complete more work in less time. Human capital and technology increases productivity because they aid the workers so that more work can be completed.

8. Refer to the chart below and explain the cause of the decrease in the output, productivity, and employment in manufacturing in the United States. What can the United States do to reverse this downward trend in manufacturing? Deregulations has more ups than downs. In this chart, the effect of not having the government involved is exemplified.

Reflection: What are two questions that you still have about these particular standards? What way would market economy be useful? How do inputs and outputs show scarcity?

2. Why has the role of government in the economy increased dramatically since the 1880s? During the 19th century, governments played a central and pervasive role both in establishing the economic and institutional conditions necessary for the occurrence of the Industrial Revolution and for promoting its spread to the follower European nations. Everywhere, governments reduced the risks of private transactions by promulgating laws that limited entrepreneurial liability, increasing the security of property rights, and enforcing private contracts.

3. Write an argument that supports or opposes the statement in the visual below that says, "deregulation won't work because people are greedy”? I believe that the deregulation wont work, because the whole purpose of starting a business is to make money. Its very little people who can say they have enough money, because you can never have enough money. And without the regulation prices will be through the roof and the workers will be mistreated an it wouldnt benefit the consumers or owner.

4. Explain why the government provides public goods and services. Why are these public goods and services NOT provided by the private sector? (Please include a discussion on non-rivalries and non-excludable goods) The government provides public good and services because they have to be non-rivalrous and non- excludable so that everyone can have access to these goods. If private sectors provided these goods, they would not be non-rivalrous and non-excludable.

5. What are the 6 functions of government in a market economy (provide an example of how the government fulfills each of these 6 functions)? The six functions of government in a market economy are freedom, security, efficiency, stability, equity, and economic growth. Freedom is achieved by the people having the freedom to work (or not), freedom to produce, trade and consume any goods and services acquired without the use of force, fraud or theft. Security is achieved by having stable income or other resources to support a standard of living now and in the foreseen future. Efficiency is achieved by production proceeding at the lowest possible per-unit cost. Stability is achieved by the absence of excessive fluctuations in the economy, an example is high employment. Economic growth is achieved when a nation’s wealth increases over time.

6. Describe the relationship that inputs and outputs have on productivity? The input is adding more capital to a business to increase the workers productivity, which will improve the business output. In additional to that also increase the company's profit.

7. How do investments in capital goods, technology, human capital, training, and educating workers, improve productivity and economic growth? You invest into capital goods, technology, human capital, training, and educating workers that improves productivity because smarter workers find ways to complete more work in less time. Human capital and technology increases productivity because they aid the workers so that more work can be completed.

8. Refer to the chart below and explain the cause of the decrease in the output, productivity, and employment in manufacturing in the United States. What can the United States do to reverse this downward trend in manufacturing? Deregulations has more ups than downs. In this chart, the effect of not having the government involved is exemplified.

Reflection: What are two questions that you still have about these particular standards? What way would market economy be useful? How do inputs and outputs show scarcity?

Saturday, August 28, 2010

Nicholas Byrd

August 13, 2010

World Issue/ Economics

*How does scarcity influence the choices you make about how you spend your money? Give a specific example of a trade-off that you had to make. What was the opportunity cost of your decision? Afterwards how did you feel about your choice? Scarcity influences me because I only have very small amount money to try to buy something expensive. I can see if I had a job that pays a good amount off money then I will be able to buy stuff that is limited up to the cost. A trade-off I had to make was going to a fancy restaurant or the mall I choose the mall because I can walk out with more merchandise. My opportunity cost was that I didn’t get to eat at Houston which is one of the best restaurants. I felt good and proud of myself because instead of going to the restaurant I went the mall and got what I wanted and more.

*How do your business owners influence each of these factors of production? What is a risk and reward that business owner might incur with each of the four factor productions? Well a Business owner Influence their land by improving opportunities to enable the business with the people you want to do business with. Labor are in short supply, which increases the costs by requiring either more pay to acquire the labor that is available, the recruiting of labor from other areas, or the usage of the less productive labor that is available locally. My Capital goods are t-shirts, shorts; pants, socks, sweaters, and shoes. Entrepreneurship this is the input to production may be thought of as good management and showing the customer’s respect.

*Do you see yourself more as an individuals that will supply labor or as an entrepreneur who make decision about the use of labor? Explain how you reached this conclusion? I see myself as an entrepreneur who makes decision about the use of labor because if my business is going the right way then there will be enough money to pay my labors.

*How do you feel about your knowledge of this standard? What are two questions that you have about this standard? I feel comfortable about this standard because I paid attention and study my vocabulary words and it helps a lot. One of my question is what is the difference between Scarcity and Opportunity cost and is there a way i can remember the four factors of productions.

August 13, 2010

World Issue/ Economics

*How does scarcity influence the choices you make about how you spend your money? Give a specific example of a trade-off that you had to make. What was the opportunity cost of your decision? Afterwards how did you feel about your choice? Scarcity influences me because I only have very small amount money to try to buy something expensive. I can see if I had a job that pays a good amount off money then I will be able to buy stuff that is limited up to the cost. A trade-off I had to make was going to a fancy restaurant or the mall I choose the mall because I can walk out with more merchandise. My opportunity cost was that I didn’t get to eat at Houston which is one of the best restaurants. I felt good and proud of myself because instead of going to the restaurant I went the mall and got what I wanted and more.

*How do your business owners influence each of these factors of production? What is a risk and reward that business owner might incur with each of the four factor productions? Well a Business owner Influence their land by improving opportunities to enable the business with the people you want to do business with. Labor are in short supply, which increases the costs by requiring either more pay to acquire the labor that is available, the recruiting of labor from other areas, or the usage of the less productive labor that is available locally. My Capital goods are t-shirts, shorts; pants, socks, sweaters, and shoes. Entrepreneurship this is the input to production may be thought of as good management and showing the customer’s respect.

*Do you see yourself more as an individuals that will supply labor or as an entrepreneur who make decision about the use of labor? Explain how you reached this conclusion? I see myself as an entrepreneur who makes decision about the use of labor because if my business is going the right way then there will be enough money to pay my labors.

*How do you feel about your knowledge of this standard? What are two questions that you have about this standard? I feel comfortable about this standard because I paid attention and study my vocabulary words and it helps a lot. One of my question is what is the difference between Scarcity and Opportunity cost and is there a way i can remember the four factors of productions.

Blog Assignment #3

1. What are the three basic economic questions that every society (economic system) must answer?

*What goods and services should be produced?

*How should the goods and services be produced?

* For whom should the goods and services be produced

2. What is an economic system? What are the four types of economic systems and how does each answer the three basic economic questions? Give one example of each. Set of principles and techniques by which a society decides and organizes the ownership and allocation of economic resources. At one extreme, usually called a free-enterprise system, all resources are privately owned. Market Economy, Command Economy, Mixed Economy, and Traditional Economy.In Traditional economy, the three economic questions are decided mainly by the social customs.Market economy is like capitalism in U.S and the economic questions are decided by individuals in the marketplace. Command economy, the questions are decided by the government. In Mixed economy,

3. Write a detailed explanation of how each of the four economic system answer the three basic question.

4. While the United States is largely a market economy, how does it also reflect a combination of economic systems. The US reflects a combination of economic systems because buyers/sellers do not make all the economic decisions. The government also plays a major role in making economic decisions. Because of the government involvement in the economy this would beb a characteristic of a command.

5. The Inuit tribe in Alaska teach their children that they must always do their best at every task. The child begins by observing the adults working on a task. When the time comes for the child to do the task, the task is first divided into smaller tasks. The adults praise the child at each stage the child successfully completes. When all stages have been complete, the child is ready takes full responsibility for the task. What economic system is used by the Inuit? Explain. Because the example describes how the Inuit tribe in Alaska teach children how to do specific tasks they are passing along customs and traditions of the tribe which are characteristic of a traditional economy.

6. How do market, command and traditional economics systems compare and contrast with each other in terms of profit motive, private ownership, consumer sovereignty, competition and government regulation? Market and Command economies focus on profit while Traditional economies focus on providing for their people. In a Market economy there is alot of private ownership while in the Command economy the government owns everything and in a Traditional economy everyone owns the businesses. In a Market economy the consumer sovereignty regulates the supply and demand. Competition is a another factor that helps regulate a the Market economy.

7.Explain why Adam Smith would oppose government intervention in a market economy. Give a specific example of why you support Adam Smith’s theories of laissez faire and the ‘invisible hand’ in a market economy and one example of why you would oppose his theory? Explain. Adam Smith opposed monopolies in the market economy . He believed that the law of supply and demand and the law of competition would regulate a free market. Adam Smith’s theories of laissez-faire described economics in terms of an "invisible hand" that regulates market economy. This means that producers will supply what consumer need most.

*What goods and services should be produced?

*How should the goods and services be produced?

* For whom should the goods and services be produced

2. What is an economic system? What are the four types of economic systems and how does each answer the three basic economic questions? Give one example of each. Set of principles and techniques by which a society decides and organizes the ownership and allocation of economic resources. At one extreme, usually called a free-enterprise system, all resources are privately owned. Market Economy, Command Economy, Mixed Economy, and Traditional Economy.In Traditional economy, the three economic questions are decided mainly by the social customs.Market economy is like capitalism in U.S and the economic questions are decided by individuals in the marketplace. Command economy, the questions are decided by the government. In Mixed economy,

3. Write a detailed explanation of how each of the four economic system answer the three basic question.

4. While the United States is largely a market economy, how does it also reflect a combination of economic systems. The US reflects a combination of economic systems because buyers/sellers do not make all the economic decisions. The government also plays a major role in making economic decisions. Because of the government involvement in the economy this would beb a characteristic of a command.

5. The Inuit tribe in Alaska teach their children that they must always do their best at every task. The child begins by observing the adults working on a task. When the time comes for the child to do the task, the task is first divided into smaller tasks. The adults praise the child at each stage the child successfully completes. When all stages have been complete, the child is ready takes full responsibility for the task. What economic system is used by the Inuit? Explain. Because the example describes how the Inuit tribe in Alaska teach children how to do specific tasks they are passing along customs and traditions of the tribe which are characteristic of a traditional economy.

6. How do market, command and traditional economics systems compare and contrast with each other in terms of profit motive, private ownership, consumer sovereignty, competition and government regulation? Market and Command economies focus on profit while Traditional economies focus on providing for their people. In a Market economy there is alot of private ownership while in the Command economy the government owns everything and in a Traditional economy everyone owns the businesses. In a Market economy the consumer sovereignty regulates the supply and demand. Competition is a another factor that helps regulate a the Market economy.

7.Explain why Adam Smith would oppose government intervention in a market economy. Give a specific example of why you support Adam Smith’s theories of laissez faire and the ‘invisible hand’ in a market economy and one example of why you would oppose his theory? Explain. Adam Smith opposed monopolies in the market economy . He believed that the law of supply and demand and the law of competition would regulate a free market. Adam Smith’s theories of laissez-faire described economics in terms of an "invisible hand" that regulates market economy. This means that producers will supply what consumer need most.

Thursday, August 26, 2010

Standards EF2 and EF3 Production Possibilities Curve;Rational Decision Making; and Specialization

Nicholas Byrd

August 26, 2010

Ms.McCray

*If you owned a business, what would a production possibilities curve tell you? Be specific. What are two factors that could cause your production possibilities curve to shift outward? It will tell me the combination of two commodities(goods, products) that can be produced efficiently with a society's available resources.

*If I was to own a business and I use the Production Possibilities Curve it would help me see which one of my products sells the most and which one sells the least.Two factors that could casue the curve to go outward is rational decisions and specialization.A PPC only shows the maximum production for two products using current resources. Also, your answer to the cause of PPC shifting outward is incorrect.

*What is the best way to determine whether or not we are making a rational economic decision? To set up a production possibilities curve and see what products are profitable.

*Why do companies choose to specialize and trade? What would happen if companies did not specialize? If a company did not specialize it would not be able to maximize production capabilities and would not be able to exploit is comparative advantage.

August 26, 2010

Ms.McCray

*If you owned a business, what would a production possibilities curve tell you? Be specific. What are two factors that could cause your production possibilities curve to shift outward? It will tell me the combination of two commodities(goods, products) that can be produced efficiently with a society's available resources.

*If I was to own a business and I use the Production Possibilities Curve it would help me see which one of my products sells the most and which one sells the least.Two factors that could casue the curve to go outward is rational decisions and specialization.A PPC only shows the maximum production for two products using current resources. Also, your answer to the cause of PPC shifting outward is incorrect.

*What is the best way to determine whether or not we are making a rational economic decision? To set up a production possibilities curve and see what products are profitable.

*Why do companies choose to specialize and trade? What would happen if companies did not specialize? If a company did not specialize it would not be able to maximize production capabilities and would not be able to exploit is comparative advantage.

*How do you feel about your knowledge of this standard?What are two questions that you have about this standard? I feel like i understand the standard I would like to Kno more about the PPC chart and want to know more about the rational decision making.

Subscribe to:

Posts (Atom)